2023 Federal Budget

On March 28, 2023, the Deputy Prime Minister and Finance Minister, the Honourable Chrystia Freeland, presented Budget 2023.

Jumping right into the top questions we have been receiving - there have been no changes to personal or corporate tax rates or to the inclusion rate on taxable capital gains. Some highlights include the following:

A. Personal Measures

Modifications to the alternative minimum tax regime focused on high-income individuals.

A one-time grocery rebate equal to two quarterly GST/HST credit payments.

Additional flexibility and possibilities with Registered Disability and Registered Education Savings Plans were introduced.

B. Business Measures

Modifications to the intergenerational business transfer rules to set requirements for activity by the children in the business and the transfer of control, equity ownership and management from the parents to the children.

Introduction of the employee ownership trust structure to provide a mechanism for business owners to transfer ownership in their private corporations to employee groups.

Several investment tax credits and other incentives were introduced or modified to encourage investment in clean energy.

C. International Measures

Confirmation of the government’s intention to introduce legislation implementing the income allocation rule and a domestic minimum top-up tax applicable to Canadian entities of multinational enterprises consistent with the OECD's BEPS initiatives.

D. Sales and Excise Tax

Increasing the air travellers security charge, limiting increases to alcohol excise duties for one year and adjusting the cannabis excise duty remittance frequency.

E. Other Measures

New income-tested dental care program for uninsured Canadians.

F. Previously Announced Measures

Intention to proceed with previously announced measures, including those related to excessive interest and financing expenses limitations; reporting rules for digital platform operators; extension of the residential property flipping rule to assignment sales; substantive Canadian-controlled private corporations; the mandatory disclosure rules; the electronic filing and certification of tax and information returns; and GST/HST changes in respect of cryptoasset mining.

The Numbers

The Government’s fiscal position includes the following projected surplus (deficit):

Surplus/(Deficit) in billions by year:

2022–2023 ($43.0) 2023–2024 ($40.1)

2024–2025 ($35.0) 2025–2026 ($26.8)

2026–2027 ($15.8) 2027–2028 ($14.0)

A. Personal Measures

Alternative Minimum Tax (AMT) for High-Income Individuals

Individuals will owe AMT if the tax amount calculated under the AMT regime is greater than the tax calculated under the ordinary progressive tax rate regime. Under the current rules, the calculation of AMT allows fewer deductions, exemptions and tax credits than under the ordinary income tax rules and applies a flat 15% tax on income over a standard $40,000 exemption.

Budget 2023 proposes several changes to the AMT calculation. First, the AMT rate is proposed to increase from 15% to 20.5%.

Second, the exemption would increase from $40,000 to the start of the fourth tax bracket (for 2024 this is approximately $173,000). Third, the AMT base would be broadened by further limiting tax preferences (i.e., exemptions, deductions and credits) as follows:

The capital gains inclusion rate would increase from 80% to 100%.

30% of capital gains eligible for the lifetime capital gains exemption would be included.

Deductions of capital loss carry forwards and allowable business investment losses would apply at a 50% rate.

100% of employee stock options benefits would be included.

30% of capital gains on donations of publicly listed securities would be included.

Only 50% of many deductions would be allowed, including the following: employment expenses (other than those incurred to earn commission income); moving expenses; child care expenses; interest and carrying charges incurred to earn income from property; northern residents deduction; and non-capital and limited partnership losses of other years.

Only 50% of non-refundable tax credits historically allowed for AMT purposes would be allowed.

The ability to recover AMT in the seven subsequent years, to the extent that tax computed under the ordinary progressive tax rate regime exceeds AMT, is not proposed to change.

The proposed changes would come into force for the 2024 personal tax year.

Grocery Rebate

Individuals and families with modest incomes receive the Goods and Services Tax Credit (GSTC). The maximum 2022/2023 GSTC is $467 for a single person, and $612 plus $161 per child for a married or common-law couple. Budget 2023 proposes a one-time payment called the Grocery Rebate which will equal half of the annual maximum (twice the quarterly payment received in January, 2023) to be paid as soon as possible after the legislation is passed.

Deduction for Tradespeople’s Tool Expenses

Under the current law, a tradesperson can claim a deduction of up to $500 of eligible new tools acquired in a taxation year as a condition of employment. Budget 2023 proposes to double the maximum employment deduction for tradespeople’s tools from $500 to $1,000, effective for 2023 and subsequent taxation years. As a consequence of this change, extraordinary tool costs that are eligible to be deducted under the apprentice vehicle mechanics’ tools deduction would be those costs that exceed the combined amount of the increased deduction for tradespeople’s tool expenses ($1,000) and the Canada employment credit ($1,368 in 2023) or 5% of the taxpayer’s income earned as an apprentice mechanic, whichever is greater.

Registered Education Savings Plans (RESPs)

Government grants and investment income can be withdrawn from RESPs as an education assistance payment (EAP) when a beneficiary is enrolled in an eligible post-secondary program. These withdrawals are taxable.

Under the current law, beneficiaries that are full-time students cannot withdraw more than $5,000 in EAPs in respect of the first 13 consecutive weeks of enrollment in a 12-month period. For part-time students, the limit is $2,500 per 13-week period. Budget 2023 proposes to increase these limits to $8,000 for full-time students and $4,000 for part-time students.

Budget 2023 also proposes to enable divorced or separated parents to open joint RESPs for one or more of their children or to move an existing joint RESP to another promoter. Under the current law, only spouses or common-law partners can jointly enter into an agreement with an RESP promoter to open an RESP.

These changes would come into force on Budget Day.

Registered Disability Savings Plans (RDSPs)

Where the contractual competence of a person with a disability who is 18 years of age or older is in doubt, the RDSP plan holder must be that person’s guardian or legal representative. A temporary measure allowed the person’s parent, spouse or common-law partner (a “qualifying family member”) to open an RDSP and be the plan holder where the person does not have a legal representative.

Budget 2023 proposes to extend this measure by three years, to December 31, 2026. Budget 2023 also proposes to broaden the definition of qualifying family members to include a brother or sister of the beneficiary who is 18 years of age or older. Qualifying family members who become a plan holder before the end of 2026 could remain the plan holder after 2026.

These proposals would apply as of royal assent of the enacting legislation.

Retirement Compensation Arrangements (RCAs)

An RCA is type of employer-sponsored arrangement that generally allows an employer to provide supplemental pension benefits to employees. A refundable tax is imposed at a rate of 50% on contributions to an RCA trust, as well as on income and gains earned or realized by the trust. The tax is generally refunded as the retirement benefits are paid to the employee. The employer receives a full deduction for contributions made to the RCA.

Employers who do not pre-fund supplemental retirement benefits through contributions to an RCA trust and instead settle retirement benefit obligations as they become due, can obtain a letter of credit (or a surety bond) issued by a financial institution in order to provide security to their employees. To secure or renew the letter of credit, the employer pays an annual fee or premium charged by the issuer. These fees and premiums are subject to the 50% refundable tax.

Budget 2023 proposes that fees or premiums paid for the purposes of securing or renewing a letter of credit (or a surety bond) for an RCA that is supplemental to a registered pension plan will not be subject to the refundable tax. This change would apply to fees or premiums paid on or after Budget Day.

Budget 2023 also proposes to allow employers to request a refund of previously remitted refundable taxes in respect of such fees or premiums paid in prior years. They would be entitled to recover 50% of retirement benefits paid after 2023, to a maximum of the refundable taxes paid in the past.

B. Business Measures

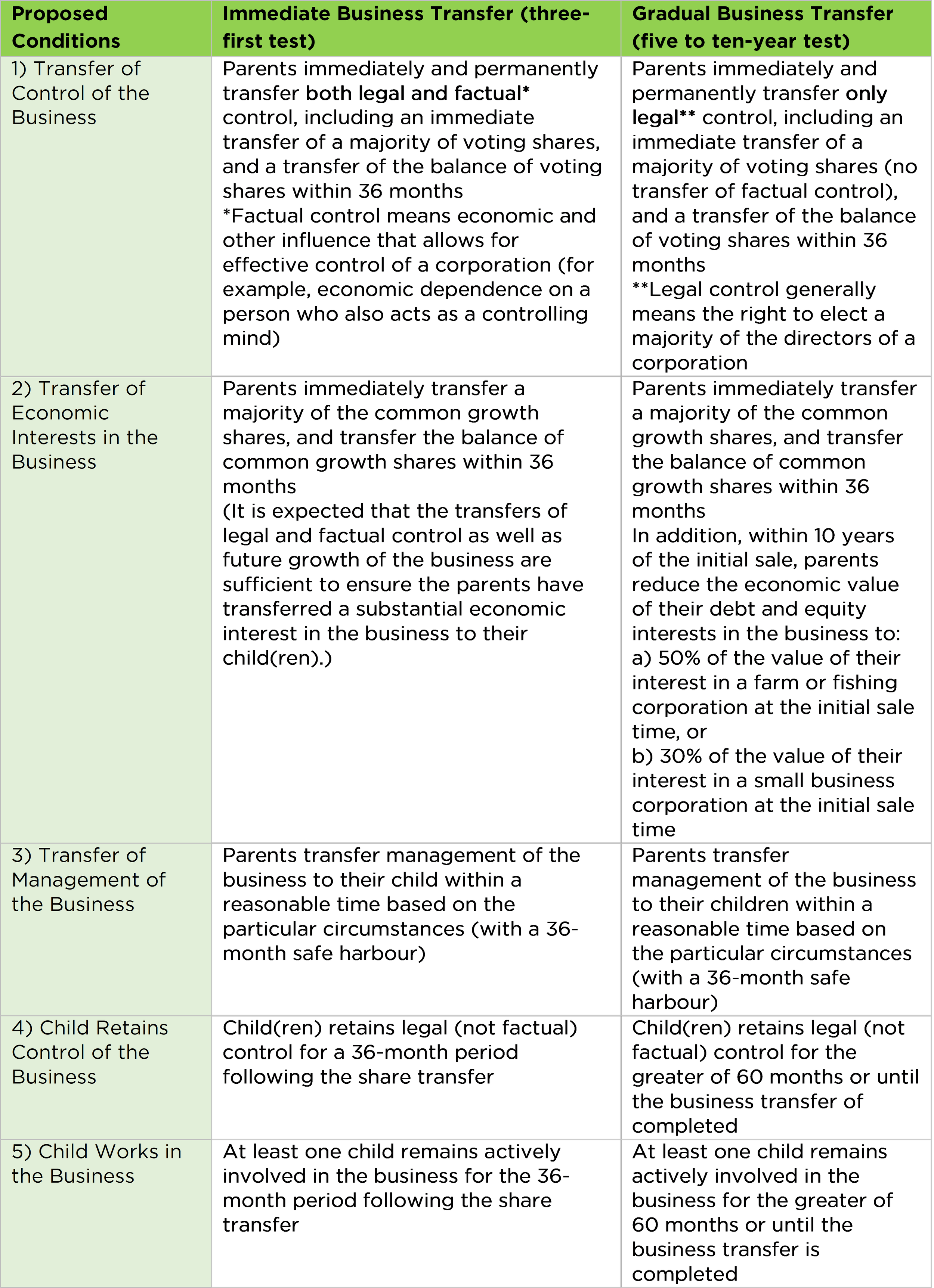

Strengthening the Intergenerational Business Transfer Framework

Historically where parents transferred shares of their corporation to a corporation owned by their children, deemed dividends rather than capital gains would arise on the disposition (due to Section 84.1 of the Income Tax Act). In 2021, legislation was passed (Bill C-208) to provide an exception from this deemed dividend treatment to facilitate the transfer of family businesses to the next generation. This exception allowed parents to utilize the lifetime capital gains exemption or simply receive capital gain treatment on the disposition, and enjoy the same tax benefits available on a sale to unrelated third parties.

However, the government was concerned that this exception contained insufficient safeguards and may have provided an inappropriate tax advantage where there was no transfer of a business to the next generation.

More specifically, this exception did not require that:

the parent cease to control the underlying business of the corporation whose shares are transferred,

the child(ren) purchasing the shares have any involvement in the business,

the interest in the purchaser corporation held by the child(ren) continue to have value, or

the child(ren) retain an interest in the business after the transfer.

Proposed Amendments

Budget 2023 proposes to amend these rules to ensure that they apply only where a genuine intergenerational business transfer (IBT) takes place.

A genuine IBT under the current law would be a transfer of shares of a corporation (the Transferred Corporation) by an individual shareholder (the Transferor) to another corporation (the Purchaser Corporation) where both of the following conditions are satisfied:

each share of the Transferred Corporation must be a “qualified small business corporation share” or a “share of the capital stock of a family farm or fishing corporation” (both as defined in the Income Tax Act), at the time of the transfer (in general terms, this requires that all or substantially all of its assets be used in an active business carried on in Canada); and

the Purchaser Corporation must be controlled by one or more persons each of whom is an adult child of the Transferor (the meaning of “child” for these purposes would include grandchildren, step-children, children-in-law, nieces and nephews, and grandnieces and grandnephews).

To ensure that only genuine IBTs are excluded from the deemed dividend rules, Budget 2023 proposes additional conditions be added. To provide flexibility, taxpayers who wish to undertake a genuine IBT may choose to rely on one of two transfer options:

an immediate business transfer (three-year test) based on arm’s length sale terms; or

a gradual business transfer (five-to-ten-year test) based on traditional estate freeze characteristics (an estate freeze typically involves a parent crystalizing the value of their economic interest in a corporation into shares that no longer share in growth in the corporate value to allow future growth to accrue to their children while the parent’s fixed economic interest is then gradually diminished by the corporation repurchasing the parent’s shares).

The immediate transfer rule would provide finality earlier in the process, though with more stringent conditions. In recognition that not all business transfers are immediate, the gradual transfer rule would provide additional flexibility for those who choose that approach.

Both the immediate and gradual business transfer options would reflect the hallmarks of a genuine IBT. The chart below outlines the proposed conditions to qualify as a genuine IBT under each option.

When the current exception was introduced, it was intended that there be restrictions for transfers of large corporations. However, these restrictions were not effectively implemented. Budget 2023 indicates that there would be no limit on the value of shares transferred in reliance upon this rule.

The current exception includes restrictions on sale of the business by the purchaser corporation within five years of the share transfer. Budget 2023 proposes that these requirements would be eliminated. In addition, new relieving rules would apply to deem requirements 3, 4 and 5 in the above chart to be met in respect of a child where either of the following occurs:

the child dies or becomes permanently disabled; or

the child disposes of their entire their interest in the business in an arm’s length disposition.

In order to benefit from the exception to the deemed dividends, the Transferor and child(ren) would be required to jointly elect for the transfer to qualify as either an immediate or gradual intergenerational share transfer. The child(ren) would be jointly and severally liable for any additional taxes payable by the Transferor on deemed dividends resulting from a transfer that does not meet the above conditions. The joint election and joint and several liability recognize that the actions of the child could potentially cause the parent to fail the conditions and to be reassessed in this regard.

The limitation period for reassessing the Transferor’s liability for tax that may arise on the transfer is proposed to be extended by three years for an immediate business transfer and by ten years for a gradual business transfer, ensuring that the Transferor can be reassessed if the requirements are not met throughout the applicable period.

Budget 2023 also proposes to provide a ten-year capital gains reserve for genuine intergenerational share transfers that satisfy the above proposed conditions, which would allow capital gains to be brought into income over a period of up to ten years, in proportion to proceeds received. The normal limit for such reserves is five years.

These rules would apply to share sales occurring on or after January 1, 2024.

Employee Ownership Trusts (EOTs)

An EOT is a form of employee ownership where a trust holds shares of a corporation for the benefit of the corporation’s employees. EOTs can be used to facilitate the acquisition by employees of their employer’s business, without requiring them to pay directly to acquire shares. This will provide business owners an additional option for succession planning. Budget 2023 proposes new rules to facilitate the use of EOTs to acquire and hold shares of a business.

The following subsections describe the general rules that would apply to EOTs. Complex requirements are set out in draft legislation included in the Budget papers.

Definitions

To be an EOT, a trust would be required to be resident in Canada (excluding deemed resident trusts) and have only two purposes. First, it would hold shares of qualifying businesses for the benefit of the employee beneficiaries of the trust. Second, it would make distributions to employee beneficiaries, where reasonable, under a distribution formula that could only consider an employee’s length of service, remuneration and hours worked. Otherwise, all beneficiaries must generally be treated in a similar manner.

An EOT would be required to hold a controlling interest in the shares of the qualifying business. A qualifying business would need to meet certain conditions. It would be required to be a Canadian-controlled private corporation. All or substantially all of the fair market value of its assets must be attributable to assets used in an active business carried on in Canada. A qualifying business would not be able to carry on business as a partner in a partnership. An EOT would not be permitted to allocate shares of a qualifying business to individual beneficiaries.

Trustees of the EOT would be elected by the beneficiaries every five years. Individuals who held a significant economic interest in a business prior to its acquisition by the EOT would not be able to make up more than 40% of the trustees of the EOT, the directors of a corporation serving as a trustee of the EOT or the directors of any qualifying business owned by the EOT. This limit would also include persons related to such individuals.

Trust beneficiaries would be limited to qualifying employees. Individuals, and persons related to them, who hold, or held prior to the disposition to the EOT, a significant economic interest in the business would be excluded from being qualifying employees.

The Tax Treatment

The EOT would be a taxable trust and will be generally subject to the same rules as other personal trusts. Therefore, undistributed trust income would be taxed in the EOT at the top personal marginal tax rate. If the EOT distributes dividends received from the qualifying business, those dividends would retain their character when received by employee beneficiaries and would be eligible for the dividend tax credit.

Qualifying Business Transfer

A qualifying business transfer would occur when a taxpayer disposes of shares of a qualifying business for proceeds that do not exceed fair market value. The shares must be disposed of to either a trust that qualifies as an EOT immediately after the sale or a corporation owned 100% by the EOT. The EOT must own a controlling interest in the qualifying business immediately after the qualifying business transfer.

Benefits

A 10-year capital gain reserve would be available, therefore allowing capital gains to be brought into income over a period of up to ten years, in proportion to proceeds received. The normal limit for such reserves is five years.

A loan from the qualifying business to the EOT for the purchase of the shares of the qualifying business could be repaid within 15 years, an exception to the usual rule that loans to a shareholder are included in income if not repaid by the end of the following fiscal year.

The EOT would be able to hold the shares indefinitely without being deemd to realize capital gains. Most trusts are deemed to realize all gains accumulated in their assets every 21 years.

These amendment would apply as of January 1, 2024.

Clean Electricity Investment Tax Credit

Budget 2023 proposes to introduce a 15% refundable tax credit for eligible investments in:

non-emitting electricity generation systems: wind, concentrated solar, solar photovoltaic, hydro (including large-scale), wave, tidal, nuclear (including large-scale and small modular reactors);

abated natural gas-fired electricity generation (which would be subject to an emissions intensity threshold compatible with a net-zero grid by 2035);

stationary electricity storage systems that do not use fossil fuels in operation, such as batteries, pumped hydroelectric storage, and compressed air storage; and

equipment for the transmission of electricity between provinces and territories.

Both new projects and the refurbishment of existing facilities will be eligible. Taxable and non-taxable entities such as Crown corporations and publicly owned utilities, corporations owned by Indigenous communities, and pension funds, would be eligible. The clean electricity investment tax credit could be claimed in addition to the Atlantic investment tax credit, but generally not with any other investment tax credit.

In order to access the tax credit in each province and territory, other requirements will include a commitment by a competent authority that the federal funding will be used to lower electricity bills, and a commitment to achieve a net-zero electricity sector by 2035.

The clean electricity investment tax credit would be available as of Budget Day 2024 for projects that did not begin construction before Budget Day 2023. The credit would not be available after 2034.

Clean Hydrogen Investment Tax Credit

Budget 2023 proposes to introduce the clean hydrogen refundable investment tax credit for investments made in clean hydrogen production based on the lifecycle carbon intensity of hydrogen (previously noted in the 2022 Fall Economic Statement). The amount of the credit, which ranges from 15% to 40%, is based on assessed carbon intensity of the hydrogen that is produced (i.e., kilogram (kg) of carbon dioxide equivalent (CO2e) per kg of hydrogen).

The credit would be available in respect of the cost of purchasing and installing eligible equipment for projects that produce hydrogen from electrolysis or natural gas (so long as emissions are abated using carbon capture, utilization, and storage).

Property that is required to convert clean hydrogen to clean ammonia would also be eligible for the credit, at the lowest credit rate of 15%.

This measure would apply to property that is acquired and that becomes available for use on or after Budget Day. The credit would be fully phased out for property that becomes available for use after 2034.

Clean Technology Investment Tax Credit

The 2022 Fall Economic Statement proposed a 30% clean technology investment tax credit for Canadian businesses adopting in clean technology and investing in eligible property that is acquired and that becomes available for use on or after Budget Day 2023. Eligible capital costs include investments in:

electricity generation systems, including solar photovoltaic, small modular nuclear reactors, concentrated solar, wind, and water (small hydro, run-of-river, wave, and tidal);

stationary electricity storage systems that do not use fossil fuels in their operation, including but not limited to: batteries, flywheels, supercapacitors, magnetic energy storage, compressed air storage, pumped hydro storage, gravity energy storage, and thermal energy storage;

low-carbon heat equipment, including active solar heating, air-source heat pumps, and ground-source heat pumps; and

industrial zero-emission vehicles and related charging or refuelling equipment, such as hydrogen or electric heavy-duty equipment used in mining or construction.

Budget 2023 proposes to expand eligibility of the tax credit to include geothermal energy systems that are eligible for Class 43.1 of Schedule II of the Income Tax Regulations. The expansion would apply in respect of property that is acquired and becomes available for use on or after Budget Day, where it has not been used for any purpose before its acquisition.

The phase-out of the credit would commence in 2034, rather than 2032 as previously announced.

Investment Tax Credit for Carbon Capture, Utilization and Storage (CCUS)

Budget 2022 proposed a refundable investment tax credit for the cost of purchasing and installing eligible equipment used in an eligible CCUS project for businesses that incur eligible expenses starting on January 1, 2022.

Budget 2023 proposes the following changes in respect of the CCUS, with details to be released in the coming months:

Dual use equipment that produces heat and/ or power or uses water, that is used for CCUS as well as another process, would be eligible for the CCUS tax credit on a pro-rated basis in proportion to the expected energy balance or material balance supporting the CCUS process over the first 20 years of the project.

British Columbia would be added to the list of eligible jurisdictions for dedicated geological storage, applicable to expenses incurred on or after January 1, 2022.

Credits related to eligible refurbishment costs incurred once the project is operating would be calculated based on the average of the expected eligible use ratio for the five-year period (the period) in which they are incurred, and each subsequent period (i.e., the periods over which they contribute to the useful life of the project).

These measures would apply to eligible expenses incurred after 2021 and before 2041.

Labour Requirements Related to Certain Investment Tax Credits

Budget 2023 proposes to implement the government’s intention to attach prevailing wage and apprenticeship requirements to the proposed clean electricity, clean technology and clean hydrogen investment tax credits. In general, the rates available for these credits will be reduced by 10% if the following labour two requirements are not met.

Wage requirement – Businesses would need to ensure that all covered workers are compensated at a level that meets or exceeds the relevant wage, plus the substantially similar monetary value of benefits and pension contributions (converted into an hourly wage format), as specified in an “eligible collective agreement.”

Apprenticeship requirement – Businesses would need to ensure that for a given taxation year, not less than 10% of the total labour hours performed by covered workers engaged in subsidised project elements be performed by registered apprentices. Covered workers are those whose duties correspond to those performed by a journeyperson in a Red Seal trade.

The requirements would apply to work performed on or after October 1, 2023. Budget 2023 also indicated that labour requirements are intended to apply to the investment tax credit for carbon capture, utilization, and storage, with details to be announced at a later date.

Clean Technology Manufacturing Investment Tax Credit

Budget 2023 proposes to introduce a 30% refundable investment tax credit for clean technology manufacturing and processing, and critical mineral extraction and processing, on the capital cost of eligible property associated with eligible activities, including:

extraction, processing, or recycling of critical minerals essential for clean technology supply chains, specifically: lithium, cobalt, nickel, graphite, copper, and rare earth elements;

manufacturing of renewable or nuclear energy equipment;

processing or recycling of nuclear fuels and heavy water;

manufacturing of grid-scale electrical energy storage equipment;

manufacturing of zero-emission vehicles; and,

manufacturing or processing of certain upstream components and materials for the above activities, such as cathode materials and batteries used in electric vehicles.

The credit would apply to property that is acquired and becomes available for use on or after January 1, 2024. The credit would be gradually phased out, starting with property that becomes available for use in 2032 and would no longer be in effect for property that becomes available for use after 2034.

Interaction of Clean Energy Investment Tax Credits

For a particular property, businesses would be able to claim only the investment tax credits for carbon capture, utilization and storage; clean technologies; clean electricity; or clean technology manufacturing. However, multiple tax credits could be available for the same project if the project includes different types of eligible property.

Zero-Emission Technology Manufacturers

In 2021, the corporate income tax rate for qualifying zero-emission technology manufacturers was reduced by 50%.

Budget 2023 proposes to expand eligible activities to include the following nuclear manufacturing and processing activities:

manufacturing of nuclear energy equipment;

processing or recycling of nuclear fuels and heavy water; and

manufacturing of nuclear fuel rods.

This expansion would apply for taxation years beginning after 2023.

Budget 2023 proposes to extend the availability of these reduced rates by three years, such that the planned phase-out would start in taxation years that begin in 2032. The measure would be fully phased out for taxation years that begin after 2034.

Tax on Repurchases of Equity

The 2022 Fall Economic Statement announced the government’s intention to introduce a 2% tax on the net value of all types of share repurchases by public corporations in Canada. Budget 2023 provides the design and implementation details of the proposed measure. The tax would apply only to public corporations (Canadian-resident corporations whose shares are listed on a designated stock exchange).

It would not apply to mutual fund corporations, but would apply to real estate investment trusts, specified investment flow-through (SIFT) trusts and SIFT partnerships if they have units listed on a designated stock exchange.

The proposed tax would apply in respect of repurchases and issuances of equity that occur on or after January 1, 2024.

General Anti-Avoidance Rule (GAAR)

The GAAR in the Income Tax Act is intended to prevent abusive tax avoidance transactions while not interfering with legitimate commercial and family transactions. If abusive tax avoidance is established, the GAAR applies to deny the tax benefit created by the abusive transaction.

A consultation on various approaches to modernizing and strengthening the GAAR has recently been conducted. A consultation paper released last August identified a number of issues with the GAAR and set out potential ways to address them. As part of the consultation, the government received a number of submissions, representing a wide variety of viewpoints.

Preamble

A preamble would be added to the GAAR, in order to help address interpretive issues and ensure that the GAAR applies as intended. While the GAAR informs the interpretation of, and applies to, every other provision of the Income Tax Act, it fundamentally denies tax benefits sought to be obtained through abusive tax avoidance transactions. It in effect draws a line: while taxpayers are free to arrange their affairs so as to obtain tax benefits intended by Parliament, they cannot misuse or abuse the tax rules to obtain unintended benefits. The preamble would also clarify that the GAAR is intended to apply regardless of whether or not the tax planning strategy used to obtain the tax benefit was foreseen.

Avoidance Transaction

The threshold for an “avoidance transaction” potentially subject to the GAAR would be reduced from a “primary purpose” test to a “one of the main purposes” test. This is consistent with the standard used in many modern anti-avoidance rules in other countries and is considered by the government to strike a reasonable balance, as it would apply to transactions with a significant tax avoidance purpose but not to transactions where tax was simply a consideration.

Economic Substance

A rule would be added to the GAAR to better meet the objective of requiring economic substance in addition to literal compliance with the words of the Income Tax Act. Currently, Supreme Court of Canada jurisprudence has established a more limited role for economic substance.

The proposed amendments would provide that economic substance is to be considered at the ‘misuse or abuse’ stage of the GAAR analysis and that a lack of economic substance tends to indicate abusive tax avoidance. A lack of economic substance will not always mean that a transaction is abusive. It would still be necessary to determine the object, spirit and purpose of the provisions or scheme relied upon, in line with existing GAAR jurisprudence. In cases where the tax results sought are consistent with the purpose of the provisions or scheme relied upon, abusive tax avoidance would not be found even in cases lacking economic substance.

The amendments would provide indicators for determining whether a transaction or series of transactions lacks economic substance. These are not an exhaustive list of factors that might be relevant and different indicators might be relevant in different cases. However, in many cases, the government believes that the existence of one or more of these indicators would strongly point to a transaction lacking economic substance. These indicators are:

whether there is the potential for pre-tax profit;

whether the transaction has resulted in a change of economic position; and

whether the transaction is entirely (or almost entirely) tax motivated.

Budget 2023 provided the example of an individual contributing to a tax-free savings account. Such a transfer could be considered to be entirely tax motivated, with no change in economic position or potential for profit other than as a result of tax savings. Even if the transfer is considered to be lacking in economic substance, it is clearly not a misuse or abuse of the relevant provisions of the Income Tax Act. The individual is using their tax-free savings account in precisely the manner that Parliament intended. There are contribution rules that specifically contemplate such a transfer and, perhaps more fundamentally, the basic tax-free savings account rules would not work if such a transfer was considered abusive.

The proposal would not supplant the general approach under Canadian income tax law, which focuses on the legal form of an arrangement. In particular, it would not require an enquiry into what the economic substance of a transaction actually is (e.g., whether a particular financial instrument is, in substance, debt or equity). Rather, it would require consideration of a lack of economic substance in the determination of abusive tax avoidance.

Penalty

A penalty would be introduced for transactions subject to the GAAR, equal to 25% of the amount of the tax benefit. Where the tax benefit involves a tax attribute that has not yet been used to reduce tax, the amount of the tax benefit would be considered to be nil. The penalty could be avoided if the transaction is disclosed to CRA, either as part of mandatory disclosure rules which are currently proposed or voluntarily.

Reassessment Period

A three-year extension to the normal reassessment period would be provided for GAAR assessments, unless the transaction had been disclosed to CRA as discussed above.

Consultation

Budget 2023 announced a consultation on these proposals to close on May 31, 2023. Following this consultation, the government intends to publish revised legislative proposals and announce the application date of the amendments.

Dividends Received Deduction by Financial Institutions

Corporations are able to deduct dividends received on shares of other corporations resident in Canada in computing their taxable income, preventing the same earnings being subject to multiple levels of corporate taxation. The government considers this treatment inconsistent with the mark-to-market rules that essentially classify gains on portfolio shares held by banks as business income. Budget 2023 proposes to deny the dividend deduction in respect of dividends received by financial institutions on shares that are mark-to-market property, effective for dividends received after 2023.

Income Tax and GST/HST Treatment of Credit Unions

A credit union (as defined for income tax and GST purposes) benefits from a GST/HST rule allowing it to receive most taxable supplies of goods and services from credit union centrals and other credit unions on an exempt basis. The definition prevents a credit union that earns more than 10% of its revenue from sources other than certain specified sources (such as interest income from lending activities) from meeting the definition of “credit union,” and qualifying for the special income tax and GST/HST rules governing credit unions.

This could arise even though the credit union’s governing legislation permits it to earn revenue from these other sources. Most credit unions are currently full-service financial institutions that offer a comprehensive suite of financial products and services. Budget 2023 proposes to eliminate the revenue test from the definition of “credit union” and amend that definition to accommodate how credit unions currently operate, effective for taxation years ending after 2016.

C. International Measures

International Tax Reform – Base Erosion and Profit Shifting

Canada is one of 137 members of the OECD/Group of 20 (G20) Inclusive Framework on Base Erosion and Profit Shifting (the Inclusive Framework) that have joined a two-pillar plan for international tax reform agreed to on October 8, 2021. Budget 2023 reiterates Canada’s commitment to the framework, and its intention to implement the Pillar One (intended to reallocate a portion of taxing rights over the profits of the largest and most profitable multinational enterprises to market countries where their users and customers are located) and Pillar Two (intended to ensure that the profits of large multinational enterprises are subject to an effective tax rate of at least 15%, regardless of where they are earned) initiatives.

Budget 2023 announces the government’s intention to introduce legislation implementing the income inclusion rule and a domestic minimum top-up tax applicable to Canadian entities of MNEs that are within scope of Pillar Two, with effect for fiscal years of MNEs that begin on or after December 31, 2023.

D. Sales and Excise Tax

Alcohol Excise

Alcohol excise duties are automatically indexed to total Consumer Price Index (CPI) inflation at the beginning of each fiscal year (i.e., on April 1st). Budget 2023 proposes to temporarily cap the inflation adjustment for excise duties on beer, spirits and wine at 2%, for one year only, as of April 1, 2023.

Cannabis Taxation – Quarterly Duty Remittances

Excise duties are imposed on cannabis products, and are generally remittable on a monthly basis. Budget 2022 brought forward a measure that allowed certain smaller licensed cannabis producers to remit excise duties on a quarterly basis. Budget 2023 proposes to allow all licensed cannabis producers to remit excise duties on a quarterly rather than monthly basis, starting from the quarter beginning on April 1, 2023.

Air Travellers Security Charge

The Air Travellers Security charge (ATSC) is generally paid by passengers when they purchase airline tickets. Budget 2023 proposes to increase ATSC rates by 32.85%, noting that these rates were last increased in 2010, at which time they were raised by 52.4%.

The proposed new ATSC rates will apply to air transportation services that include a chargeable emplanement on or after May 1, 2024, for which any payment is made on or after that date. The charge for a domestic one-way flight will rise from $7.48 to $9.94. The transborder charge will increase from $12.71 to $16.89, and the charge for other international travel will increase from $25.91 to $34.42. These rates include the GST or federal portion of HST.

E. Other Measures

Small Business Credit Card Fees

Budget 2023 announced that commitments had been obtained from Visa and Mastercard to lower fees for small businesses. More than 90% of credit card-accepting businesses are expected to see their fees reduced by up to 27%.

Automatic Tax Filing for Low-income Canadians

Budget 2023 announced that the number of Canadians eligible for CRA’s automatic File My Return service will be increased to 2 million by 2025, almost tripling the number of currently eligible Canadians. In 2022, 53,000 returns were filed using this service. In addition, a new pilot project will be implemented to assist vulnerable Canadians in applying for benefits even if they do not file tax returns.

Student Benefits

Budget 2023 proposes increasing Canada student grants by 40%, raising the interest-free Canada student loan limit from $210 to $300 per study week, and waiving the requirement for mature students (aged 22 or older) to undergo credit screening in order to qualify.

Dental Care for Canadians

The Canadian dental care plan would provide coverage for all uninsured Canadians with an annual family income of less than $90,000 (the Canada dental benefit only provided benefits for children under 12) by the end of 2023. The plan will be administered by Health Canada with support from a third-party benefits administrator. Benefits are reduced for families with income between $70,000 and $90,000.

Protecting Federally Regulated Gig Workers

Budget 2023 proposes to amend the Canada Labour Code to strengthen prohibitions against employee misclassification for federally regulated gig workers such that they will receive protections and benefits including EI and CPP.

Ensuring the Integrity of Emergency COVID-19 Benefits

Budget 2023 proposes to provide $53.8 million in 2022-23 to Employment and Social Development Canada to support integrity activities relating to overpayments of COVID-19 emergency income supports.

F. Previously Announced Measures

Budget 2023 confirms the government’s intention to proceed with the following previously announced tax and related measures, as modified to take into account consultations and deliberations since their release.

Legislative proposals released on November 3, 2022 with respect to Excessive Interest and Financing Expenses Limitations and Reporting Rules for Digital Platform Operators.

Tax measures announced in the Fall Economic Statement on November 3, 2022, for which legislative proposals have not yet been released, including: automatic advance for the Canada workers benefit; investment tax credit for clean technologies; and extension of the residential property flipping rule to assignment sales.

Legislative proposals released on August 9, 2022, including with respect to the following measures:

borrowing by defined benefit pension plans;

reporting requirements for Registered Retirement Savings Plans (RRSPs) and Registered Retirement Income Funds (RRIFs);

fixing contribution errors in defined contribution pension plans;

the investment tax credit for Carbon Capture, Utilization and Storage;

hedging and short selling by Canadian financial institutions;

substantive Canadian-controlled private corporations;

mandatory disclosure rules;

the electronic filing and certification of tax and information returns;

Canadian forces members and veterans amounts;

other technical amendments to the Income Tax Act and Income Tax Regulations proposed in the August 9th release; and

remaining legislative and regulatory proposals relating to the Goods and Services Tax/Harmonized Sales Tax, excise levies and other taxes and charges announced in the August 9th release.

Legislative proposals released on April 29, 2022 with respect to hybrid mismatch arrangements.

Legislative proposals released on February 4, 2022 with respect to the Goods and Services Tax/Harmonized Sales Tax treatment of cryptoasset mining.

Legislative proposals tabled in a Notice of Ways and Means Motion on December 14, 2021 to introduce the Digital Services Tax Act.

The transfer pricing consultation announced in Budget 2021.

The income tax measure announced on December 20, 2019 to extend the maturation period of amateur athletes trusts maturing in 2019 by one year, from eight years to nine years.

Measures confirmed in Budget 2016 relating to the Goods and Services Tax/Harmonized Sales Tax joint venture election.